For most homeowners in Texas, asking if foundation repair is covered by insurance often leads to a frustrating answer: “It depends.” The short answer is usually no, but there are some really important exceptions you need to know about.

Standard policies are designed to cover sudden, accidental damage—not the slow-moving, gradual sinking and cracking that our infamous expansive clay soils are known for.

Does Homeowners Insurance Cover Foundation Repair

Trying to make sense of a homeowners insurance policy can feel like you’re reading a foreign language, especially when the stakes are as high as your home’s foundation. The whole idea behind these policies is to shield you from unexpected disasters, not to pay for the predictable wear and tear that comes with owning a home.

Think of it like this: your policy is a bodyguard for your house, ready to jump in when something sudden and unexpected happens. It’s built to cover damage from specific events, which insurance companies call “covered perils.” These are the specific disasters listed in your contract.

When it comes to foundation coverage, it almost always boils down to one simple question: Was the damage sudden and accidental, or did it happen slowly over time? Insurers nearly always deny claims for gradual problems because they see it as a maintenance issue, not an accident.

Understanding Covered Perils

So, what kind of sudden events could actually get your foundation repair covered? While every policy is a bit different, a standard HO-3 policy—which is what most Americans have—typically covers damage from things like:

- Fire or lightning: If a fire tears through your home and weakens the foundation, the repairs should be covered.

- Explosions: A gas leak explosion or a similar catastrophic event is a textbook example of a covered peril.

- Vehicle impact: If a car loses control and smashes into your house, damaging the foundation, your policy is there to help.

- Sudden water damage: This is a big one. If a pipe bursts under your slab foundation, washing away the supporting soil and causing a sudden shift, that’s often covered. This is completely different from a slow, dripping leak or general dampness.

The Reality of Claim Denials

Unfortunately, the things that cause most foundation problems here in Texas—like our shifting clay soil, intense droughts, and gradual house settling—are almost always listed as specific exclusions in standard policies.

The numbers don’t lie. Industry data shows that issues from earth movement and gradual settling make up about 80% of all foundation claims filed each year. Because of those policy exclusions, only about 15-20% of these claims ever get approved. The ones that do are almost always tied to a clear, sudden event like a burst pipe. You can dig deeper into these global foundation repair service market trends to see the financial side of things.

This hard truth often shocks homeowners who believe their insurance is a safety net for any major home repair. Knowing this upfront can save you a lot of frustration and help you figure out the best course of action if you start seeing cracks appear.

Foundation Damage Insurance Coverage At a Glance

To make it easier, here’s a quick breakdown of what’s typically covered and what’s not when it comes to foundation damage in Texas.

| Damage Cause | Typically Covered? | Why or Why Not? |

|---|---|---|

| Gradual Settling & Shifting Soil | No | Policies exclude “earth movement” and view this as a preventable maintenance issue. |

| Drought or Poor Drainage | No | This is considered a slow, gradual process, not a sudden and accidental event. |

| Faulty Construction | No | Standard policies don’t cover poor workmanship; that’s an issue for the builder. |

| Sudden Water Line Break (Under Slab) | Yes | This is often considered a “covered peril” because the damage was sudden and accidental. |

| Flooding (from external sources) | No | Requires a separate flood insurance policy; standard homeowners policies exclude flood damage. |

| Fire or Explosion | Yes | These are classic examples of covered perils that can cause structural damage. |

This table is just a general guide, of course. The specific language in your own policy is what ultimately matters, but this gives you a good idea of how insurers look at these situations.

Understanding Your Policy’s Exclusions

Before you can figure out if your foundation repair is covered by insurance, you have to get familiar with your policy’s “exclusions” section. This is where the insurance company spells out, in no uncertain terms, what they won’t pay for. Honestly, this fine print is the single biggest reason most foundation claims in Texas get denied.

It helps to think of your homeowners insurance like a car warranty. The warranty covers a sudden engine failure but won’t pay for new tires after 50,000 miles, rust from leaving the car out in the rain, or damage from never getting an oil change. Insurance companies look at your foundation the same way—they’re interested in sudden, unexpected events, not slow decline.

So, let’s grab a magnifying glass and look at the “Big Three” exclusions that stop most homeowners in their tracks.

Gradual Soil Settlement and Earth Movement

This is, without a doubt, the number one reason claims get denied here in North Texas. Our area is known for its expansive clay soil. When it gets wet, it swells up like a sponge; when it dries out, it shrinks. This constant cycle of expanding and contracting puts tremendous stress on your foundation, year after year.

Because this process is slow, predictable, and ongoing, insurers lump it under their “earth movement” exclusion. From their perspective, dealing with shifting soil is just part of routine home maintenance, not a sudden accident they need to cover. That means those hairline cracks that have been slowly getting bigger over the years due to seasonal soil changes? They’re almost never covered.

Normal Wear and Tear

Your foundation, just like your roof or your water heater, gets old. Over the decades, concrete can develop minor cracks and materials can start to break down. Standard homeowners insurance is designed to be a safety net for unexpected disasters, not to fight the inevitable effects of time.

Here’s the bottom line: insurance is not a home maintenance plan. If an adjuster looks at the damage and decides it’s simply a result of the house getting older, they will deny the claim under the “wear and tear” exclusion.

This rule exists to prevent people from using insurance to pay for home improvement projects or to fix problems that could have been avoided with a little proactive upkeep.

Faulty Construction or Poor Workmanship

But what if the problem isn’t time or soil, but the way your house was built in the first place? Unfortunately, your homeowners policy won’t step in here, either. Issues like a builder who didn’t compact the soil properly, used cheap concrete, or had a flawed design are all considered “faulty construction.”

Insurance is there to protect you from unforeseen events, not to fix another professional’s mistakes. If you find yourself in this situation, your only real option is to go after the builder’s warranty (if it’s still active) or pay for the repairs yourself.

Other Common Foundation Exclusions

Beyond those main three, your policy likely has a list of other specific things it won’t cover. Knowing these can save you a ton of time and frustration.

- Pest Damage: Termites and other wood-destroying pests can absolutely wreck a pier and beam foundation. However, insurance carriers see this as a preventable maintenance issue, so it’s specifically excluded.

- Earthquakes: While major quakes are rare in DFW, any ground shaking from seismic activity is a standard exclusion. You’d need a separate earthquake insurance policy for that kind of protection.

- Flooding: This is a big one. Water damage from a pipe that bursts inside your house is completely different from a natural flood. Damage caused by rising creeks, overflowing rivers, or a major storm surge is only covered if you have a separate flood insurance policy, usually from the National Flood Insurance Program (NFIP) or a private company.

Getting a handle on these exclusions is your most important first step. It gives you realistic expectations and helps you focus on the cause of the damage—because when it comes to insurance, that’s the only thing that truly matters.

When Your Foundation Repair Is Actually Covered

So, when does insurance actually step in? It’s a frustrating question, but the answer is simpler than you might think. The trick is to stop focusing on the damage—the cracks and the sinking floors—and start looking at the cause.

Insurance companies draw a hard line between gradual problems and sudden, accidental events. If you can prove the root cause was something unexpected that happened all at once (what they call a “covered peril”), you’ve got a solid case for coverage.

Think of it like this: your foundation is a dinner plate. If it slowly gets a hairline crack from years of being washed and used, that’s just normal wear and tear. But if you accidentally drop a heavy pot on it and it shatters? That’s a sudden event. Insurance is there to cover the dropped pot, not the slow aging process.

Sudden and Accidental Water Damage

In Texas, one of the most common covered events we see is a major plumbing failure. I’m not talking about a slow drip under your bathroom sink. I mean a catastrophic burst that unleashes a ton of water right where it can do the most damage.

Imagine a water line buried under your slab foundation suddenly gives way. The high-pressure water can literally blast away the soil supporting your home in just a few hours. This can cause a whole section of your house to heave or drop abruptly. This is a textbook example of a covered peril because the damage was both sudden and accidental. The foundation work needed to fix this mess would almost certainly be covered by your policy.

Other Clear-Cut Covered Perils

Beyond plumbing blowouts, a few other events leave little room for an insurance company to argue. The cause is external, immediate, and obviously not something you could have prevented with regular maintenance.

Here are a few real-world examples that usually result in an approved claim:

- Fire: The intense heat from a house fire can cause concrete to crack and spall, completely wrecking its structural integrity.

- Explosions: A natural gas leak that ignites can send powerful shockwaves through the ground, causing instant and severe foundation damage.

- Vehicle Impact: It happens more than you’d think. A car veering off the road and hitting your home can easily crack or shift the foundation from the sheer force.

- Falling Objects: If a huge tree comes down in a storm and crashes into your house, that impact can transfer enough force to damage the foundation below.

The key takeaway here is that in each of these situations, the foundation damage is just one piece of a larger, covered disaster. The insurance company’s job is to restore your home to how it was before the event, and that absolutely includes making the foundation solid again.

The Evolution of Foundation Coverage

It’s interesting to see how much things have changed over the years. Back in the 1980s, policies were a lot more generous. Historical data shows they covered up to 40% of settling claims under a pretty broad definition of “collapse.”

Fast forward to 2023, and those approvals have plummeted to under 10% due to much stricter policy language. This change lines up with the growth of the foundation repair market itself—it went from $2.47 billion in 2020 to an estimated $2.83 billion in 2024. More homeowner awareness and an uptick in severe weather have fueled this boom.

From our own experience, about 70% of our insurance-assisted jobs involve helping homeowners connect the dots after a storm or flood, often leveraging specific water damage riders in their policies to get the claim approved. You can read more about the growing foundation repair services market and how it ties into these insurance trends.

At the end of the day, your best tool is knowing the difference between gradual foundation cracks and settling versus sudden, catastrophic damage. Once you can identify the true cause, you’ll know whether it’s worth filing that claim. You can learn more about how to distinguish between these issues in our guide on identifying serious foundation cracks and settling.

A Step-by-Step Guide to Filing Your Claim

Staring down an insurance claim can feel like you’re standing at the base of a mountain. It looks overwhelming, but the way to the top is one step at a time. Breaking the process down into manageable chunks is the key to navigating it successfully and getting your foundation repair covered.

The single most important rule? Act fast, but document everything first. Before you touch a thing or start any cleanup, your first job is to become a crime scene investigator. Your mission is to capture the scene exactly as you found it, creating undeniable proof of the damage.

Step 1: Document Everything—Immediately

Think of it as building a case file for your insurer. The stronger and more detailed your evidence, the tougher it is for them to argue with your claim. Right now, your smartphone is your best friend.

- Take Way More Photos Than You Think You Need: Get pictures from every conceivable angle. Snap close-ups of the cracks, pull back for wide shots of the entire affected area, and don’t forget related damage like cracked drywall or doors that suddenly won’t close right.

- Record a Walk-Through Video: A video adds context that static photos can miss. As you record, narrate what you’re seeing, pointing out the specific problems and mentioning when you first noticed them.

- Jot Down Detailed Notes: Create a timeline. When exactly did you find the damage? What was happening around that time—a massive thunderstorm, a burst pipe? The more specific your notes are, the better.

This initial evidence is the bedrock of your entire claim. Without it, you’re just relying on memory, and the insurance company is relying on their adjuster’s interpretation, which might not see things your way.

Step 2: Notify Your Insurance Company

With your first round of evidence gathered, it’s time to make the call. Don’t put this off. Most policies insist that you report a loss “promptly” or “as soon as reasonably possible.” Waiting too long could give the insurance company an easy reason to deny your claim.

Have your policy number handy when you call. Explain what happened clearly and stick to the facts you’ve documented. Avoid guessing about the cause or how much repairs might cost. The agent will open a claim and give you a claim number—write it down and keep it somewhere safe.

Pro Tip: Right after you hang up, send a follow-up email summarizing the conversation. This creates a paper trail, confirming when you reported the damage and what was discussed. It can be a lifesaver later on.

Step 3: Prepare for the Adjuster’s Visit

The insurance adjuster is the person assigned to investigate your claim. Their role is to assess the damage, figure out the cause, and estimate the repair cost based on what your policy covers. Your job is to make their job easy by being completely prepared.

Have all your documentation—photos, videos, notes—ready for their review. It’s also a massive advantage to have a professional assessment in hand before they even arrive. We provide the detailed reports adjusters need to see, and you can learn more about our expert assistance with insurance claims support.

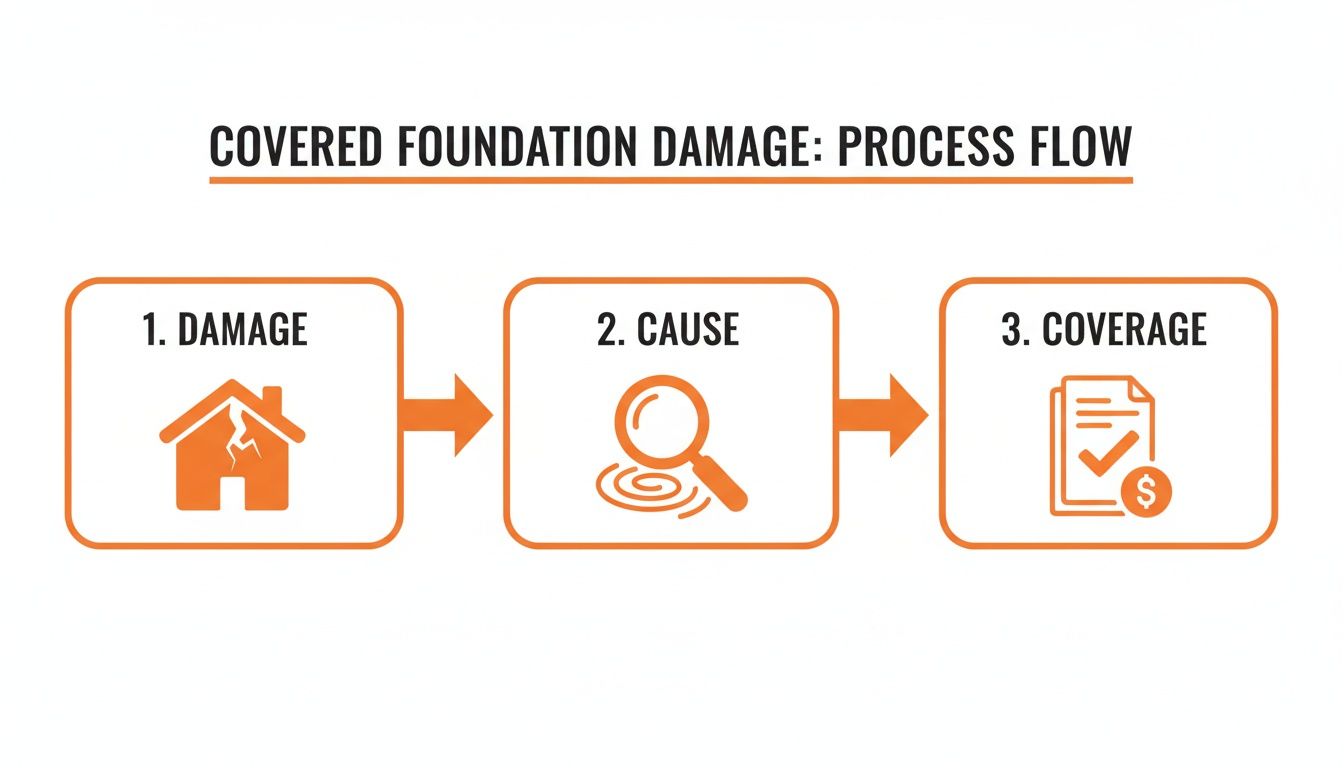

An insurer’s process is pretty straightforward: they look at the damage, investigate the cause, and then decide if it’s a covered event.

This simple flow is exactly why proving a sudden, accidental cause is the secret to getting your foundation repair covered by insurance.

It’s also a smart move to have your own contractor—like one of our specialists from Black Beard Foundation Repair—present during the adjuster’s inspection. Our expert can point out critical details the adjuster might otherwise miss and provide a real-world repair estimate to ensure nothing gets overlooked.

Step 4: Review the Settlement Offer

After the investigation, the insurance company will send you a settlement offer. This document breaks down what they believe is covered, what isn’t, and the total amount they’re willing to pay, minus your deductible.

Never feel pressured to accept the first offer on the spot. Take your time and review it carefully. Does it actually cover the full scope of repairs needed? Is the amount fair when compared to the professional estimates you’ve gotten? If the offer seems too low or you believe they’ve wrongly denied part of your claim, you absolutely have the right to negotiate or appeal. This is where having a detailed professional report gives you the leverage you need to fight for a fair settlement.

To help you stay organized, here is a simple checklist you can follow throughout the process.

Your Foundation Damage Insurance Claim Checklist

| Step | Action Item | Pro Tip from Black Beard Foundation Repair |

|---|---|---|

| 1. Damage Discovery | Take extensive photos and videos of the damage before any cleanup. Write down a detailed timeline of events. | Don’t just focus on the foundation. Document related issues like cracked walls, uneven floors, and sticking doors. |

| 2. Policy Review | Locate your homeowners insurance policy. Read the sections on “covered perils” and “exclusions.” | Look for language related to “sudden and accidental” water damage, collapse, or earth movement. |

| 3. Initial Contact | Call your insurance agent or the claims hotline to report the damage. Get your claim number. | After the call, send a follow-up email to create a written record of your initial report. Keep it brief and factual. |

| 4. Professional Inspection | Schedule an inspection with a reputable foundation repair company like Black Beard to get an expert assessment and repair estimate. | Having our detailed report before the adjuster arrives gives you a powerful baseline for negotiations. |

| 5. Adjuster Meeting | Prepare all your documentation for the adjuster’s visit. Be present during their inspection. | Have us there with you. We can speak the same language as the adjuster and point out crucial evidence they might miss. |

| 6. Settlement Review | Carefully read the settlement offer. Compare it against your professional estimate and your policy coverage. | Don’t cash the check if you disagree with the offer. Cashing it can be seen as accepting their terms. |

| 7. Negotiation/Appeal | If the offer is too low, submit a counter-offer with your professional report as evidence. | Stay professional and persistent. Clearly state why you believe their assessment is inaccurate and provide your supporting documents. |

| 8. Resolution | Once you agree on a fair settlement, you can proceed with scheduling the repairs. | Keep meticulous records of all communications, expenses, and repair invoices until the claim is officially closed. |

Following these steps methodically will keep you in control of the process and give you the best possible chance of getting the full and fair settlement you deserve.

How a Professional Can Strengthen Your Claim

Trying to navigate an insurance claim on your own can feel like you’re fighting an uphill battle. This is where a trusted foundation repair expert becomes your most valuable ally, providing the hard evidence and professional expertise to level the playing field.

Think of us as your translator and advocate. We speak the technical language adjusters understand and can build a case that’s hard to ignore.

When an insurance adjuster shows up, they’re looking for objective, verifiable proof of a covered event. While your own photos and notes are a great start, a detailed report from a qualified professional is the true cornerstone of a successful claim.

Providing Expert Documentation and Estimates

Our free, unbiased foundation evaluations are designed to do more than just spot a problem. We create a comprehensive report that documents the full extent of the damage, pinpoints the most likely cause, and lays out a precise, line-item repair plan. This isn’t just a quote; it’s a professional assessment that gives your claim serious credibility.

Our team is well-versed in spotting damage from covered perils like hidden plumbing leaks or storm-related soil shifts. Making that distinction is absolutely critical—it can be the one thing that determines whether your foundation repair is covered by insurance.

An adjuster is far more likely to approve a claim when it’s backed by a clear, professional diagnosis that directly links the damage to a covered event. Vague assumptions are easy to dismiss, but a detailed report from a certified specialist is tough to argue with.

A thorough estimate is equally important. We provide the kind of detailed cost breakdown adjusters need to see, making sure every part of the job is accounted for, from materials and labor to any required engineering oversight.

Leveraging Local Knowledge and Experience

Working in North Texas means we know the unique challenges our expansive clay soils present. That local insight is a huge advantage. The global foundation repair services market, valued at around $3 billion in 2023, is expected to reach $4.11 billion by 2028. Much of that growth is happening right here in areas like Dallas-Fort Worth, where expansive clays contribute to 60% of structural claims each year, even though standard policies often won’t cover them. This has created a huge need for specialists who know how to handle these specific issues. You can read more about the foundation repair services market trends on futuremarketinsights.com.

Our deep understanding of these local soil conditions allows us to explain to adjusters exactly how a covered event—like a sudden water line break—would impact your foundation differently than gradual settlement. This context can be the key that unlocks your coverage.

Over the years, our team has worked with countless insurance companies and adjusters across the DFW area. We know what they look for, the questions they’ll ask, and the kind of documentation they need to sign off on a claim. That familiarity helps streamline the whole process, cutting down on the back-and-forth and getting you the coverage you deserve much faster. Figuring out the right time to bring in an expert is a crucial step, and you can learn more by reading our guide on when to call a professional for foundation repairs in Texas.

Answering Your Top Questions About Foundation Repair and Insurance

Trying to figure out insurance coverage for foundation repairs can feel like reading a foreign language. It’s confusing, and the stakes are high. Let’s clear up some of the most common questions we hear from Texas homeowners every day.

Does Flood Insurance Cover Foundation Damage?

Yes, but there’s a big catch. Your standard homeowners policy won’t touch damage from natural flooding—that’s a hard-and-fast exclusion. For that, you need a separate flood insurance policy, usually from the National Flood Insurance Program (NFIP) or a private carrier.

This is the policy that kicks in when a storm surge, overflowing river, or heavy runoff washes away the soil supporting your foundation or creates enough hydrostatic pressure to crack the concrete. It’s designed specifically to cover direct physical damage from a flood.

Here’s the critical detail: you can’t wait until the storm clouds are gathering to buy it. Most flood policies have a 30-day waiting period before they become active. So, for anyone living in the flood-prone parts of Dallas-Fort Worth, getting this coverage well in advance isn’t just a good idea—it’s your only real defense against rising waters.

If you ever need to file a claim, your camera will be your best friend. Snap photos of the floodwaters around your house and then take detailed pictures of the foundation damage as soon as the water goes down. This creates a clear timeline that directly links the flood to your foundation problems.

What Should I Do If My Claim Is Denied?

Getting that denial letter in the mail is a gut punch, but don’t assume it’s the final word. A denial is just the insurance company’s first move based on their side of the story. You absolutely have the right to push back if you believe they got it wrong.

First, read the denial letter from top to bottom. It should spell out exactly why they denied the claim and point to the specific language in your policy they’re using to justify it. You can’t argue your case until you understand theirs.

Now, it’s time to build your own case. If they’re blaming gradual settlement, your job is to prove the damage was sudden and tied to a covered event. This is where getting a professional on your side becomes a game-changer.

- Get an Independent Report: Bring in a licensed structural engineer or a reputable foundation repair company (like us) for an unbiased assessment. A detailed report from an expert that contradicts the insurance adjuster’s opinion is incredibly powerful.

- Organize Your Evidence: Pull together every photo, video, and professional report into one neat package. The more organized and thorough you are, the more credible your appeal will be.

Once you have this new evidence, you can submit a formal appeal. Write a clear, concise letter explaining why you disagree with their decision and attach all your supporting documents. If you’re still hitting a wall, you might think about bringing in a public adjuster—they work for you, not the insurance company, and can be a huge help in negotiating a fair settlement.

Will a Foundation Claim Increase My Insurance Premium?

That’s the million-dollar question, isn’t it? And the honest answer is: maybe. Filing any claim has the potential to raise your rates when it’s time to renew, but it’s not a given.

Insurance companies look at a lot of different things when setting your premium—your personal claim history, the specific type of claim, and even what’s happening with claims in your general area. A single claim, especially after a massive storm that hit half the neighborhood, is less likely to cause a big spike. The insurer expects to pay out a lot of claims after something like that.

What really gets their attention is a pattern of frequent claims. If you’ve filed several claims in a few years, they’ll start to see you as a higher risk, and your premium will almost certainly go up. The kind of claim matters, too. A major foundation repair from a burst pipe is viewed differently than a handful of small, unrelated claims.

Before you pick up the phone to file, do a little math. How much is your deductible? How much will the repair cost? If the repair is only a few hundred dollars more than your deductible, it might make more sense to pay for it yourself. That way, you keep your claims history clean and your rates stable.

At the end of the day, you have to weigh the pros and cons. For a massive, budget-breaking repair that is clearly covered, that’s exactly what insurance is for. For the smaller stuff, think about the long-term cost of a rate hike versus the short-term relief of a claim payment.

Wrestling with an insurance claim is the last thing you need when you’re already stressed about your foundation. You don’t have to go it alone. The team at Black Beard Foundation Repair has the expertise to provide the detailed inspections and professional reports that can make or break your claim. If you’re in the Dallas-Fort Worth area and need an honest assessment, contact us today for a free evaluation.